Thanks to a Guardian story based on a FoI request we now know that Treasury has modelled changes to HELP debt repayment times under Job-ready Graduates. They are six years too late to influence the original policy, but better that than never as JRG remains a live issue.

Treasury used much more sophisticated methods than my own recent analysis of arts graduate repayment prospects. However, Treasury does not use the new student debt repayment system introduced in 2025-26, and so under-estimates current repayment times. I will return to this, but Treasury has produced a helpful conceptual and empirical guide to what the Morrison government should have considered prior to Job-ready Graduates being proposed, and the Albanese government should think about when redesigning the system.

Debt and income data

Instead of just using debt levels based on three years of the relevant student contributions for each course, Treasury put into their model actual subjects taken, with data from the Department of Education included in PLIDA. So the model captures extra debts caused by double degrees, changing courses or failing and repeating subjects. It also captures lower debts of people who never complete a course.

My analysis used Australian citizen median income by single year of age, as recorded using ATO and DSS income linked to Census records. For years 1 to 10 after university Treasury used a model based on actual debtor income in PLIDA (which also has ATO and DSS data). These are critical years for repayment for most debtors, so this is important. Treasury’s model uses Census data to estimate repayments after 10 years.

Scale of debt

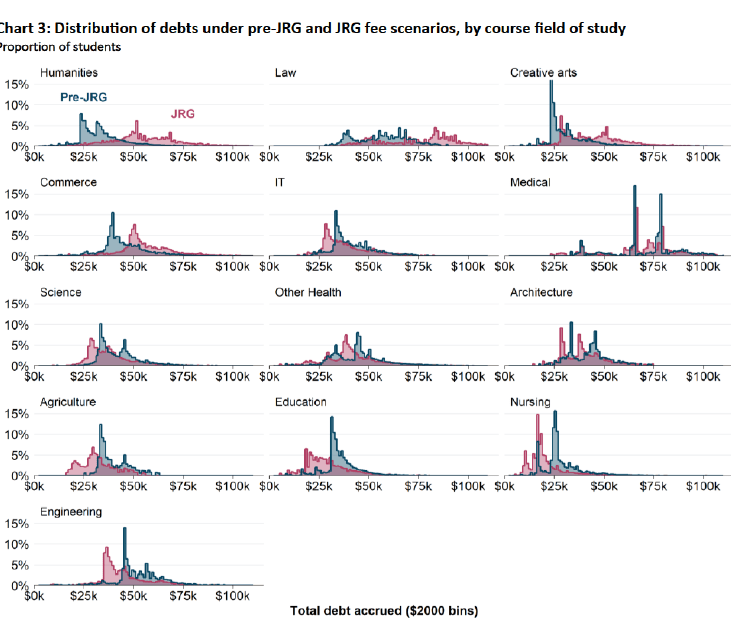

The chart below shows ranges of debt levels by field of education. We can see that under JRG a significant proportion of humanities debtors have estimated debts in the $50,0000-$75,000 range, and for law in the $75,000-$100,000 range, probably due to double degrees. Despite commerce students sharing student contributions with arts and law their total debts cluster more sharply around the $50,000 mark, with lower shares than arts moving into the $50,0000-$75,000 range. Lower rates of further study for commerce compared to humanities graduates may explain this difference.

For science, engineering, IT, nursing, and teaching we can see the range of debts shifting down, consistent with their reduced student contributions under Job-ready Graduates.

Time to repay

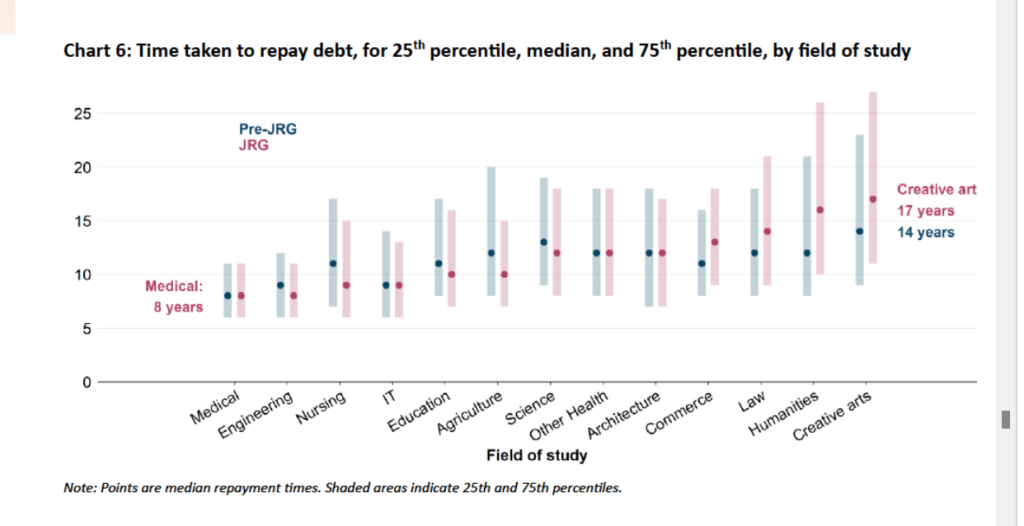

The chart below shows estimated repayment times with pre-JRG compared to post-JRG student contribution rates at different positions in the repayment sequence. For example, the 25th percentile is the number of years at which a quarter of debtors have repaid, the median at which half of debtors have repaid, and the 75th percentile at which three-quarters have repaid.

As I understand the methodology on calculating the underlying debt, the inclusion of students who don’t complete would shorten repayment times, while the inclusion of students who take more than one degree would lengthen repayment times.

On this methodology half of humanities debtors would have repaid in what looks like 11 or 12 years pre-JRG but in 16 years at JRG rates. A quarter of humanities debtors have repayment times stretching beyond 25 years.

Why the results understate repayment times

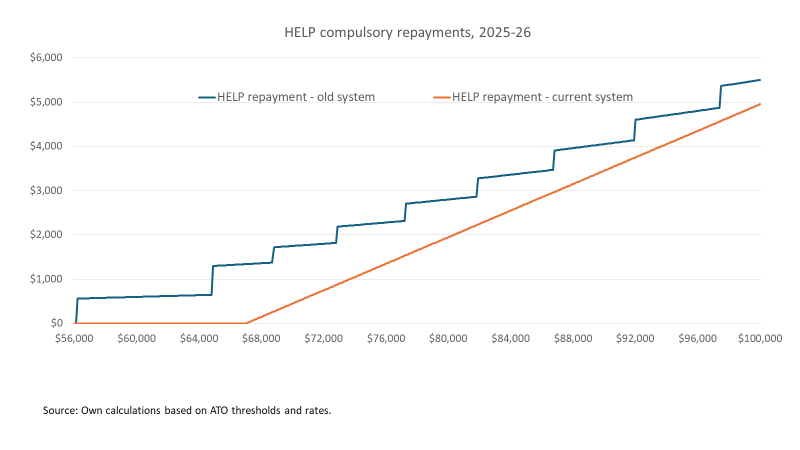

The repayment model is based on legislation as of December 2024, before the new HELP repayment system was legislated in 2025. Its key elements were 1) increasing the income threshold at which repayments start from $56,156 to $67,000 and 2) Moving from a total income approach – so repaying a % of all income earned, with the % increasing with income – to a marginal income approach, which for most HELP debtors means 15% of income above the threshold.

This change provided cost-of-living relief but also reduced annual repayments in common early career salary ranges. This slows down repayments, both through the lower amounts repaid each year and higher compound indexation on remaining debt.

The conceptual approach

I’ve thought for a long time that there could be merit in using estimated repayment times more broadly in the higher education funding system.

The basic intuition is that narrowing the range of median repayment years between disciplines creates more equality of effort in repaying student debt, despite sometimes significant differences in total debt accrued and annual salaries.

While for practical university-funding reasons student contributions should still be charged on an annual EFTSL basis, the system would take account of varying typical debts on completion, such as through degrees having different lengths.

As this Treasury paper shows, JRG went in the opposite direction. It reduced repayment times in fields which already had relatively low times and increased them in fields which already had relatively high times.

As the Treasury paper also shows, this came at a cost to the government with the student debt subsidy rate increasing. So JRG was bad for the personal finances of many student debtors and bad for public finances.

If this information was available to Cabinet when it considered JRG would they have made the same decision? Quite possibly not.

Thanx very much for this most helpful analysis.

I note further that Treasury estimates that Jobs Ready Graduates increased the subsidy rate from 27% to 29%, about half due to higher overall fees, and half due to increasing debts for students with worse repayments (pages 19-20).

LikeLike